2019 Section 342 Report to Congress

FDIC CONTRACTING: Inclusion of Minority- and Women-Owned Businesses (MWOBs)

EMPLOYMENT AT THE FDIC: Fair Inclusion of Minorities and Women

Under the provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA), Section 342, the Federal Deposit Insurance Corporation (FDIC), Office of Minority and Women Inclusion (OMWI) is required to submit to Congress an annual report regarding the actions taken by the agency toward contracting with qualified minority- and women-owned businesses and hiring qualified minority and women employees.

The FDIC is pleased to submit this 2019 Report to Congress. The report describes the FDIC’s activities relating to the inclusion of minorities and women in contracting and hiring for the year, and other relevant information, including the agency’s financial institutions diversity and contractors’ workforces fair inclusion programs and activities supporting financial access, economic inclusion, and financial literacy. Consistent with the provisions of Section 342 of the DFA, the FDIC continues to enhance its longstanding commitment to promote diversity and inclusion in employment opportunities and all business areas of the FDIC. This report outlines both accomplishments and challenges in contracting and hiring as the agency works to ensure that these efforts are reflected in its operations.

Commitment to Diversity and Inclusion

The mission of the FDIC is to preserve and promote public confidence in the U.S. financial system by insuring deposits, examining and supervising financial institutions for safety and soundness and consumer protection, making large and complex financial institutions resolvable, and managing receiverships. OMWI is an important component in these efforts and supports the FDIC’s mission through the pursuit of equal employment opportunity, affirmative employment initiatives, diversity and inclusion, and outreach efforts to ensure the fair inclusion and utilization of minority- and women-owned businesses, law firms, and investors in contracting and investment opportunities. OMWI works closely with other FDIC organizations, divisions, and offices to carry out these important responsibilities and realize program accomplishments.

When the FDIC Board of Directors established OMWI in 2011, the Board also established the FDIC Diversity and Inclusion Executive Advisory Council (EAC), to promote the Chairman’s goal of a culture of diversity and inclusion. The EAC is chaired by the FDIC Deputy to the Chairman and Chief Operating Officer and membership includes the OMWI Director, FDIC division and office directors, and other key FDIC senior staff. The EAC assists and advises decision-makers throughout the FDIC, working with OMWI, in connection with all diversity and inclusion efforts.

The Chairman’s Diversity Advisory Council (CDAC), consists of FDIC employees that serve as a means for employees to communicate to management on broad-based diversity concerns and issues. The CDAC consists of regional and area councils. The chair of each regional council serves on the Executive CDAC. The Executive CDAC advises the FDIC Chairman through the OMWI Director on diversity and inclusion issues and concerns raised by employees. This structure provides FDIC leadership with a bottom up perspective on diversity and inclusion and promotes employee engagement. The issues with proposed recommendations are presented to the EAC and then distributed to the divisions and offices for review. Following this review process OMWI collaborates with the EAC on proposed actions to address each of the recommendations. Through the CDAC FDIC leverages the differences and strengths of all employees to create a more inclusive work environment.

The FDIC’s ability to fulfill its mission is due in large-part to the commitment and dedication of the FDIC workforce. While there has been an uptick in retirements the FDIC continued its commitment to diversity and inclusion for recruiting and retaining the most qualified, talented, and motivated employees in the labor market. During 2019, FDIC implemented structural changes to the entry level-examiner hiring program to further strengthen the ability to attract, retain, and advance a diverse pool of candidates.

Also in 2019, the FDIC continued to award a high percentage of contract work to minority- and women-owned businesses, law firms, and diverse attorneys despite the downward trend in contracting activity. This successful outreach to majority-minority professional and trade organizations was conducted to expand the pipeline of qualified vendor sources. In addition, the FDIC continued to monitor and report on procurement strategies and MWOB contracting initiatives at regular EAC meetings attended by senior managers from FDIC divisions and offices.

Further, the FDIC continued to promote the economic inclusion of minority-majority communities through initiatives aimed at providing greater transparency to the public on performance, and reducing unnecessary regulatory burdens for community banks. The FDIC leadership is engaged in efforts to promote increased focus on low- andmoderate income communities through expanded engagement through Community Reinvestment Act technical assistance and Minority Depository Institutions so they are in a better position to serve their communities. Also, the FDIC continued outreach efforts to promote the safe adoption of additional products and services to bring underserved communities more fully into the banking mainstream.

2019 Diversity and Inclusion Initiatives

The FDIC is committed to continually providing all employees with a work environment that promotes excellence and acknowledges and honors the diversity of its employees. In 2019 the FDIC initiated the process to update its Diversity and Inclusion Strategic Plan (D&I Strategic Plan). The updated plan will cover a three-year period from 2020 through 2022. It includes embedding diversity and inclusion into the agency’s policies, practices, and procedures, aligning with business goals, and increasing management accountability at all levels. As in the past, the EAC will oversee the implementation of the plan and ensure that the FDIC’s commitment to diversity and inclusion remains a top priority.

Annually, each FDIC division and major office assesses available workforce data and produce plans with strategies intended to further their diversity progress and address any issues. These plans are consolidated into an FDIC Plan to promote diversity and inclusion through increased engagement with divisions and major offices. During 2019, OMWI met with each FDIC division to review diversity and inclusion statistics and discuss methods to accomplish planned actions moving forward.

In recognition of the FDIC’s 2019 diversity and inclusion accomplishments, the following initiatives are highlighted:

- The FDIC and National Treasury Employees Union (NTEU) reached an agreement regarding a new Compensation Agreement, which includes six weeks of paid parental leave for the birth, adoption, or foster care of a child. The CDAC played a critical role in bringing this issue to light for FDIC management during its briefing to the FDIC Chairman and EAC members in 2018.

- The FDIC continued to support and encourage the formation of Employee Resource Groups (ERGs). The ERGs are networks of employees with similar interests, shared characteristics or life experiences, whose goals and objectives facilitate the creation and maintenance of a work environment that recognizes, appreciates, and encourages the utilization of the talents, skills, and perspectives of all employees in the achievement of the FDIC’s mission.

- The FDIC monitored completions of Diversity 101 online training implemented in 2018, and as of the end of 2019 achieved a completion rate of over 50 percent. The OMWI Director recorded a video message posted on the intranet and “Lunch and Learn” sessions were held to encourage training completion.

- FDIC enhanced its commitment to diversity and inclusion (D&I) through engaging external D&I consulting support and training services.

- A few FDIC Divisions began utilizing D&I vendor’s services to train their managers and supervisors on unconscious bias and micro-inequities.

- The biennial CDAC Training Conference was held in Arlington, Virginia, and participants included CDAC members from headquarters, regional, and area offices. The D&I training topics included emotional intelligence, unconscious biases and micro-inequities, and engaging everyone in diversity and inclusion.

The FDIC places a high priority on achieving diversity in all business activities including contracting. OMWI is an integral part of the contractor solicitation, education, and evaluation process through conducting outreach and market research to identify qualified MWOBs for contracting opportunities with the FDIC. Through partnerships with trade organizations, OMWI has expanded its pipeline to identify MWOB firms for requirements. For 2019, FDIC awarded 152 contracts to MWOB firms with a total value of $173.5 million or 31.3 percent of all new awards.

During 2019, the FDIC implemented new contracting initiatives and conducted focused outreach which improved MWOB participation in its contracting activities. As a result of the FDIC’s outreach engagement, the corporation continued to award a high percentage of contracts to MWOB firms. Despite, challenges faced by the FDIC in increasing the utilization and growth rates for MWOB contractors because new contract awards have been declining since the height of the financial crisis and non-financial goods and services contracts for recurring needs represent a larger percentage of FDIC contracts. The FDIC will continue to analyze future contracting needs to determine where MWOB opportunities may exist and if new procurement strategies can be used to maximize MWOB participation. The following sections provide detailed information on the 2019 contracting activities and successes; contracting initiatives, programs, and outreach; and challenges the FDIC faces in increasing MWOB participation in its contracting activities.

Contracting Activities and Successes

FDIC Procurement Policies

The FDIC’s contracts are typically awarded through a competitive, best-value solicitation process that involves consideration of both the offeror’s technical and price proposals. The solicitations describe what offerors must include in their proposals and the proposal evaluation criteria specific to the good or service being procured. Proposals are evaluated and rated by a panel of FDIC subject matter experts and may include an OMWI representative. Awards are made to the offeror that provides the best value to the FDIC.

For any contract over $100,000, OMWI review is required to identify competitive minority- and women-owned businesses to include in contract solicitations. As part of this process, OMWI uses the FDIC’s Contractor Resource List (CRL) that includes registered MWOBs. The CRL is the principal database for vendors interested in doing business with the FDIC. OMWI also identifies qualified MWOBs through outreach, the System for Award Management, and the Minority Business Development Agency. This process helps ensure that a diverse pool of contractors is solicited and considered for each major contract.

The FDIC’s website1 provides extensive information, announcements, and technical assistance for minority- and women-owned businesses, law firms, and investors seeking to do business with the FDIC. The FDIC also has a small business resource page that contains about 40 learning modules2 and is a technical assistance aid and self-assessment for businesses interested in competing for contract opportunities.

1. See www.fdic.gov/about/diversity/mwop/index.html.

2. See www.fdic.gov/about/diversity/sbrp/index.html.

Contract Payments with MWOBs

The FDIC paid $466.6 million to contractors in 2019 under 1,162 contracts, of which $98.3 million (21.1 percent) was paid to MWOBs under 287 contracts. [See Figure 1.] By comparison, the FDIC paid $429.6 million to contractors under 1,299 contacts in 2018; $414.0 million to contractors under 1,537 contracts in 2017; $415.2 million to contractors under 1,786 contracts in 2016; and $507.2 million to contractors under 2,029 contracts in 2015. The 2019 total payments (i.e., spend) to contractors included payments for contracts awarded in 2019 and payments for active contracts awarded prior to 2019.

| Figure 1 Contracting Payments (in millions) | |||||

|---|---|---|---|---|---|

| 2015 | 2016 | 2017 | 2018 | 2019 | |

| Total | $507.2 | $415.2 | $414.0 | $429.6 | $466.6 |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | |

| MWOB | $142.5 | $111.5 | $109.6 | $98.0 | $98.3 |

| 28.1% | 26.8% | 26.5% | 22.8% | 21.1% | |

| Minority Owned (MO) | $89.3 | $56.0 | $54.6 | $49.5 | $54.0 |

| 17.6% | 13.5% | 13.2% | 11.5% | 11.6% | |

| Women Owned (WO) | $83.2 | $66.8 | $66.9 | $59.5 | $52.0 |

| 16.4% | 16.1% | 16.2% | 13.9% | 11.2% | |

| Overlap (Both MO & WO) | $30.0 | $11.3 | $11.9 | $11.1 | $7.7 |

| 5.9% | 2.8% | 2.9% | 2.6% | 1.7$ | |

| Asian American | $39.9 | $33.5 | $30.1 | $28.8 | $31.5 |

| 7.9% | 8.1% | 7.2% | 6.7% | 6.8% | |

| Black American | $13.3 | $11.5 | $14.2 | $9.5 | $6.2 |

| 2.6% | 2.8% | 3.4% | 2.2% | 1.3% | |

| Hispanic American | $25.1 | $10.3 | $9.5 | $8.4 | $12.0 |

| 5.0% | 2.5% | 2.3% | 2.0% | 2.6% | |

| Native American | $0.1 | $0.1 | $0.2 | $2.2 | $3.9 |

| 0.0% | 0.0% | 0.1% | .05% | 0.8% | |

For purposes of contract payment information, the FDIC considers an active contract one in which payments were made or credits applied in the same year. In 2019, minority-owned firms were paid $54.0 million of the total dollars paid to MWOB contractors (11.6 percent). Women-owned firms were paid $52.0 million of the total dollars paid to contractors (11.2 percent). These two categories – minorities and women – are not mutually exclusive since $7.7 million (1.7 percent) was paid in 2019 to businesses classified as both minority-owned and women-owned. The FDIC paid MWOBs $98.0 million (22.8 percent) of the total paid to all contractors in 2018 under 299 contracts; $109.6 million (26.5 percent) of the total paid to all contractors in 2017 under 354 contracts; $111.5 million (26.8 percent) of the total paid to all contractors in 2016 under 461 contracts; and $142.5 million (28.1 percent) of the total paid to all contractors.

In 2019, the FDIC awarded 152 contracts to MWOBs out of a total of 518 issued (29.3 percent). [See Figure 2.] By comparison, the FDIC awarded 166 contracts (29.4%) to MWOBs out of a total of 565 issued in 2018; 210 contracts (28.5 percent) to MWOBs out of a total of 737 issued in 2017; 287 contracts (24.3 percent) to MWOBs out of a total of 1,181 issued in 2016; and 346 contracts (29.9 percent) to MWOBs out of a total of 1,159 issued in 2015.

| Figure 2 Contracting Actions | ||||||

|---|---|---|---|---|---|---|

| 2015 | 2016 | 2017 | 2018 | 2019 | ||

| Total | 1159 | 1181 | 737 | 565 | 518 | |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | ||

| MWOB | 346 | 287 | 210 | 166 | 152 | |

| 29.9% | 24.3% | 28.5% | 29.4% | 29.3% | ||

| Minority Owned (MO) | 148 | 142 | 100 | 87 | 68 | |

| 12.8% | 12.0% | 13.6% | 15.4% | 13.1% | ||

| Women Owned (WO) | 243 | 187 | 151 | 119 | 112 | |

| 21.0% | 15.8% | 20.5% | 21.1% | 21.6% | ||

| Overlap (Both MO & WO) | 45 | 42 | 41 | 40 | 28 | |

| 3.9% | 3.5% | 5.6% | 7.1% | 5.4% | ||

| Asian American | 56 | 62 | 63 | 54 | 33 | |

| 4.8% | 5.2% | 8.6% | 9.6% | 6.4% | ||

| Black American | 35 | 24 | 22 | 11 | 15 | |

| 3.0% | 2.0% | 3.0% | 1.9% | 2.9% | ||

| Hispanic American | 39 | 48 | 4 | 11 | 15 | |

| 3.4% | 4.1% | 0.5% | 1.9% | 2.9% | ||

| Native American | 1 | 2 | 7 | 6 | 5 | |

| 0.1% | 0.2% | 1.0% | 1.1% | 1.0% | ||

| Other | 17 | 6 | 4 | 5 | 6 | |

| 1.5% | 0.5% | 0.5% | 0.9% | 1.1% | ||

As of December 31, 2019, the FDIC had 256 (22.3 percent) active contracts with MWOBs out of a total of 1,150 active contracts. The active contracts to MWOB firms by category were as follows: Asian American (68), Black American (24), Hispanic American (20), Native American (8), and Women (180). These include contracts awarded to firms that were both minority-owned and women-owned.

Contract Awards with MWOBs

The FDIC awarded contracts with a combined value of $554.0 million in 2019, of which $173.5 million (31.3 percent) were awarded to MWOBs. By comparison, the FDIC awarded contracts with a combined value of $499.5 million in 2018, with $122.5 million (24.5 percent) awarded to MWOBs; $523.7 million in 2017, with $96.7 million (18.5 percent) awarded to MWOBs; awarded contracts with a combined value of $508.8 million in 2016, with $93.9 million (18.5 percent) awarded to MWOBs; and awarded contracts with a combined value of $858.4 million in 2015, with $211.6 million (24.7 percent) awarded to MWOBs. [See Figure 3.]

| Figure 3 Total Contract Dollar Awards | |||||

|---|---|---|---|---|---|

| 2015 | 2016 | 2017 | 2018 | 2019 | |

| Total | $858.4 | $508.8 | $523.7 | $499.5 | $554.0 |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | |

| MWOB | $211.6 | $93.9 | $96.7 | $122.5 | $173.5 |

| 24.7% | 18.5% | 18.5% | 24.5% | 31.3% | |

| Minority Owned (MO) | $145.2 | $56.5 | $66.7 | $45.8 | $106.0 |

| 16.9% | 11.1% | 12.7% | 9.2% | 19.1% | |

| Women Owned (WO) | $104.2 | $47.4 | $46.2 | $83.0 | $75.8 |

| 12.1% | 9.3% | 8.8% | 16.6% | 13.7% | |

| Overlap (Both MO & WO) | $37.8 | $10.0 | $16.2 | $6.3 | $8.3 |

| 4.3% | 1.9% | 3.0% | 1.3% | 1.5% | |

| Asian American | $51.8 | $25.0 | $31.2 | $33.9 | $83.1 |

| 6.0% | 4.9% | 6.0% | 6.8% | 15.0% | |

| Black American | $30.7 | $9.4 | $32.7 | $1.9 | $5.8 |

| 3.6% | 1.9% | 6.2% | 0.4% | 1.0% | |

| Hispanic American | $43.2 | $20.6 | $1.6 | $7.0 | $13.3 |

| 5.0% | 4.0% | 0.3% | 1.4% | 2.4% | |

| Native American | $- | $0.1 | $0.9 | $2.9 | $3.5 |

| 0.0% | 0.0% | 0.2% | 0.6% | 0.6% | |

| Other | $19.5 | $1.4 | $0.3 | $0.1 | $0.3 |

| 2.3% | 0.3% | 0.0% | 0.0% | 0.1% | |

The FDIC’s five-year trend from 2015 – 2019 of contract awards and payments can be found at Appendix A.

Contract Awards by North American Industry Classification System

The North American Industry Classification System (NAICS) was developed by the Office of Management and Budget (OMB) and is the standard used by federal statistical agencies in classifying business establishments for the purpose of collecting, analyzing, and publishing statistical data related to the U.S. business economy. The FDIC awarded contracts in 2019 under 68 different NAICS codes. Figure 4 depicts the FDIC’s 2019 contracts categorized for the top ten NAICS codes and percentage of the total award value ($554.0 million).

Figure 4 FDIC 2019 Contracts by Top Ten NAICS Codes

In 2019, these awards consisted of the following: 21 percent for computer systems design services; 18 percent for security guards and patrol services; 14 percent for other computer related services; 10 percent for administrative management and general management consulting services; and 10 percent for software publishers. The remaining 27 percent – each eight percent or under – was awarded in the areas of commercial banking (eight percent); custom computer programming services (six percent); facilities support services (five percent); electronic computer manufacturing (five percent); and internet publishing and broadcasting and web search portals (three percent). Collectively, 32.9 percent of the top ten NAICS code contracts were awarded to MWOBs. [See Figure 5.]

Figure 5 2019 Contract Awards by Top 10 NAICS

The 2019 FDIC contract awards associated with the top ten NAICS codes can be found in Appendix B.

Legal Contracting Diversity

The Legal Division’s legal contracting program endeavors to maximize the participation of both minority- and women-owned law firms (MWOLFs) and minority and women partners and associates employed at majority owned firms (Diverse Attorneys) in legal contracting. This approach is consistent with the provisions of Section 342 of the DFA that encourages diversity and inclusion at all levels. FDIC legal matters provide important learning and professional client development opportunities to MWOLFs and Diverse Attorneys that can be quite meaningful to career advancement. In 2019, FDIC paid $10.8 million to MWOLF firms and Diverse Attorneys combined, out of a total of $31.7 million dollars paid to outside counsel. As a result, the Legal Division has an aggregate 34.0 percent diversity and inclusion participation rate in legal contracting for the year 2019. [See Figure 6.] This number represents a significant increase from 2018, in which there was a 26.5 percent aggregate participation rate, despite the decline in overall outside counsel spending.

Figure 6 2019 Participation Rate of

MWOLFs and Diverse Attorneys (in Millions)

Referrals to Minority and Women Owned Law Firms

Referrals to law firms are typically made on a competitive basis. Price, expertise, capacity, and diverse status are among the criteria considered in making the selections. The FDIC made 62 referrals to outside counsel in 2019, of which 20 (32.3 percent) were to MWOLFs, compared to a total of 104 referrals, of which 29 (28 percent) were to MWOLFs in 2018. Referrals to MWOLFs in 2019, by category, were as follows: Black American – 1 (1.6 percent), Hispanic American – 12 (19.4percent), Native American – 1 (1.6 percent), and Women – 6 (9.7 percent) [See Figure 7.]

Figure 7 2019 Number of Referrals to MWOLFs by Category

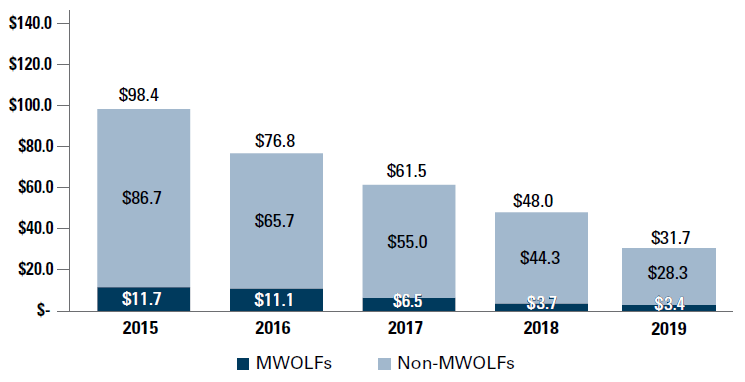

Bank resolution activities are a major source of outside counsel work, and that activity continued a downward trend in 2019. The decrease in bank resolution activity is consistent with the overall decline in FDIC fees spent on outside counsel since the near peak levels in 2014. [See Figure 8.] In 2019, the FDIC paid $31.7 million to outside counsel, as compared to $48.0 million in 2018. The FDIC paid $3.4 million to MWOLFs in 2019, which represents 10.7 percent of the total fees paid to all law firms. Notwithstanding the overall decline in bank resolution activities, the 2019 percentage of fees paid to MWOLFs is above that of 2018, during which the FDIC paid a total of $3.7 million to MWOLFs, which was 7.7 percent of the total paid to all law firms that year.

Figure 8 Historical Trend: Payments to Law Firms (in millions)

Despite the corresponding decline in the absolute number of referrals to all outside counsel in 2019 (from 104 in 2018 to 62 in 2019), there was an increase in the percentage of referrals to MWOLF firms in 2019 over 2018 (32.3 percent versus 28 percent in 2018). FDIC maintains a long-term commitment to increasing the level of referrals and fees paid to MWOLFs and Diverse Attorneys in 2020 and beyond. The Legal Division remains alert to changing circumstances, as well as diversity and inclusion leading practices and periodically recalibrates its outreach efforts to account for the same.

Referrals to Diverse Attorneys

Section 342 of the DFA encourages the FDIC to develop and implement standards and procedures to ensure, to the maximum extent possible, the fair inclusion and utilization of minorities and women in contracting at all levels. Another benefit of FDIC’s diversity and inclusion efforts in legal contracting is the training and professional development opportunities afforded minority and women partners and associates who work on FDIC legal matters that are referred to majority owned law firms. The employment and training of individual Diverse Attorneys contributes significantly toward enhancing diversity and inclusion in the legal profession by providing opportunities for drafting legal documents, entering court appearances, and developing client relationships, all of which further the partnership potential of Diverse Attorneys.

In 2019, Diverse Attorneys at majority- owned law firms billed $7.4 million on FDIC legal matters or 23.3 percent of total payments to outside counsel. [See Figure 9.] Despite the Legal Division’s diminishing annual expenditures on outside counsel services, FDIC referrals to outside counsel offer a consistently high level of learning and professional development opportunities to both MWOLFs and Diverse Attorneys. The Legal Division will continue to promote this participation and monitor these fees in addition to those fees paid to MWOLF firms.

Figure 9 2019 Fees Billed by Diverse Attorneys at Majority Law Firms

(in Millions)

Outreach to MWOLFs and Diverse Attorneys

The cornerstone of the Legal Division diversity and inclusion outreach is the FDIC’s partnerships with minority bar associations and specialized stakeholder organizations. In 2019, the FDIC Legal Division participated in seven minority bar association conferences and three stakeholder events in support of maximizing the participation of MWOLFs and Diverse Attorneys in FDIC legal contracting. The Legal Division divided its stakeholder event participation into 1) events concentrating on outreach to MWOLFs; 2) events focusing on outreach to Diverse Attorneys who work at majority owned law firms; and 3) events geared to the recruitment of individual diverse attorneys to join the FDIC workforce.

The Legal Division recognizes the value of integrating FDIC in-house attorneys in its legal contracting diversity and inclusion program activities. Therefore, the Legal Division makes a conscious effort to include FDIC attorneys in external outreach events such as bar association conferences and stakeholder meetings in order to make its outreach encounters more meaningful. In 2019, the National Association of Minority and Women Owned Law Firms (NAMWOLF) again formally recognized the FDIC as a principal member of, and major contributor to, its Inclusion Initiative, a collaborative program among law departments of major corporations designed to increase the participation of MWOLF firms in legal contracting. The FDIC participates in the Inclusion Initiative along with major corporations. The Legal Division and OMWI participated in and sponsored NAMWOLF’s National Conference.

The Legal Division’s objective is to promote diversity and inclusion in its legal contracting opportunities by producing measurable results. In 2019 the Legal Division continued to work closely with in-house attorneys in areas that account for a substantial dollar amount of legal referrals and posed the greatest opportunities for MWOLF and Diverse Attorney participation. The Legal Division held a Diversity and Inclusion in Legal Contracting Outreach Workshop in the FDIC Dallas Regional Office for in-house FDIC attorneys, who assign work to outside counsel. The program included a review of the prior year’s diversity statistics, planned projects, questions and answers, and the solicitation of ideas from the attorneys for improving the selection and retention of outside counsel.

The Legal Division evaluated and approved three new MWOLF applications in 2019. Firms from various geographic areas were added to the FDIC List of Counsel Available in order to be eligible to receive legal contracting work. In addition to the outreach efforts noted above, the Legal Division continues to provide technical assistance to other related government agencies on developing diversity and inclusion outreach programs that mirror FDIC’s program.

Legal Division Diversity and Inclusion Assessments

Pursuant to Section 342 of the DFA, which requires an assessment of legal contractors’ internal workforce diversity practices, the Legal Division refined and continued to implement a system of compliance reviews of the top billing law firms (both majorityowned and MWOLFs). This program provides the Legal Division with an additional means to address diversity and inclusion and provides opportunities for minority and women attorneys seeking to provide services. These on-site assessment visits are designed to engage firms in discussions about diversity leading practices, staffing concepts, metrics and the Legal Division’s diversity and inclusion program. The assessment results continue to show progress toward increase diversity and inclusion. In addition to collecting baseline diversity metrics, the FDIC’s Legal Division remains abreast of innovative diversity strategies, new opportunities for inclusion, pursuant to this program. Further, the Legal Division obtained commitments with various firms to increase diverse staffing on FDIC legal matters.

As a result of the assessments, the FDIC Legal Division enjoys open dialogue and transparency with external law firms on their diversity and inclusion practices. One noteworthy practice firms routinely engage in is supporting diversity pipeline programs such as the Leadership Council on Legal Diversity to strengthen the number of diverse law students entering the legal profession. Another noteworthy practice is firms are establishing scholarship programs geared toward assisting diverse law students pay for school. In addition, FDIC has noted diverse associates have entered the law firm partnership ranks as a result of having worked on FDIC legal matters.

Contracting Initiatives, Programs and Outreach

The FDIC awarded 518 new contracts with a combined value of $554.0 million in 2019. The number of new contracts awarded in 2019 represents the fewest number of awarded contracts by the FDIC since 2008. The total contract award dollars in 2019 of $554.0 million represents the fourth consecutive year the FDIC has awarded less than $600 million in new contracts. The FDIC awarded an average of 1,762 contracts with a combined average value of $1.9 billion on an annual basis from 2009-2012 during the height of the financial crisis when 440 banks failed during this period. As stated in prior reports, the FDIC annual contract awards have fallen dramatically since the height of the financial crisis due to a significant reduction in annual bank failures. During the financial crisis, contracts related to services required to resolve failed banks represented up to 85 percent of all FDIC contract dollars awarded in a given year. In 2019, only 15.6 percent of FDIC total contract dollars awarded supported the FDIC’s Division of Resolutions and Receiverships (DRR) in their mission to resolve failed banks. Despite reduced contract awards in 2019, 29.3 percent of all new contracts and 31.3 percent of all new contract dollars were awarded to MWOBs.

With fewer bank failure related contracts, FDIC continues to focus on identifying contracting opportunities for MWOBs in non-financial goods and services requirements. For example, contracts were awarded to MWOBs in the following areas: Information Technology (IT) consulting, software development and maintenance services; audit and risk management services; IT hardware, software and maintenance; training services; facilities management services; emergency preparedness services; construction management services; translation services; diversity consulting and training services.

Since 2015, the FDIC has continued its strategy to re-bid the financial services contracts as they expire to ensure contractor resources are in place when needs arise and to maintain a constant state of readiness. Although, there were only four bank failures in 2019, the FDIC continued to include MWOBs in the procurement process for these contract opportunities that arose. Several of the contracts used to perform failed bank resolution services expired in 2019.

MWOB contractors were instrumental to the FDIC’s success during the financial crisis. As a result, the FDIC focused on ensuring MWOB participation in the re-competition of these expiring contracts, as well as contracts for financial services that previously were not required. MWOB firms were awarded new contracts in 2019 for real estate services and accounting services that will be used to support future bank failures. Additional existing failed bank resolution contracts will expire in 2020 and beyond. The FDIC will continue to identify opportunities to include MWOBs in the re-competition of these mission critical services. In addition, the FDIC continued to award task orders to MWOBs under existing contracts in 2019 to support 2019 bank failures, planning for future bank failures and for services to resolve bank failures from prior years.

In 2019, the FDIC also strategically used the 8(a) set-aside program to award seven contracts with a combined value of $15.4 million to 8(a) MWOBs. Three of these contracts were for critical IT business intelligence services and amounted to $9.3 million. The other four contracts involved IT support services and proofreading of translated material.

The FDIC has also focused on soliciting MWOB firms as prime contractors that were once subcontractors to larger firms under FDIC contracts once they have gained valuable experience as a subcontractor. Throughout the last several years this strategy has resulted in many former MWOB subcontractors becoming FDIC prime contractors providing critical facilities management services, IT services and bank closing related services.

The FDIC continued to discuss procurement strategies and MWOB contracting initiatives at regular EAC meetings attended by senior managers from FDIC divisions and offices. The FDIC also continued to implement the recommendation to hold pre-proposal conferences to ensure businesses understand the FDIC’s requirements before a solicitation is issued and to give smaller businesses opportunities to find partners and develop teams before submitting bids.

Information Technology Contracting

The FDIC recognized in 2012 that the declining number of bank failures would result in a significant shift in new contract award opportunities from bank resolution contracts to contracts for daily operations (e.g., IT software development and maintenance, facilities management, etc.). The FDIC conducted focused market research in 2012 to ensure significant MWOB participation in the then upcoming $546.8 million competitive Basic Ordering Agreement (BOA) for the second generation Information Technology Application Services (ITAS II) contract which was awarded in 2013. In 2016, additional firms were competitively added to the ITAS II BOA. Currently, seven of the 14 firms (50 percent) under the ITAS II BOA are MWOBs. Only one in four firms (25 percent) under the prior ITAS I BOA was an MWOB. The assignment of work to contractors under the ITAS II BOA is accomplished through the award of task orders that are competed among the contractors awarded the BOA. Nine of the 23 task orders awarded under ITAS II in 2019 were awarded to MWOBs with a combined value of $56.8 million. This represented 39.1 percent of the total task orders awarded and 42.0 percent of the $135.3 million in total task order dollars awarded. The services provided under the task orders awarded to MWOBs in 2019 were for mission critical services to develop, maintain and enhance the FDIC’s IT systems.

ITAS II is not the only contract that supports the FDIC’s IT program. During 2019, FDIC made the strategic decision to develop certain identified mission critical new systems on a common platform. A $15.5 million contract was awarded to an MWOB firm to establish the new common platform and an $18.0 million contract was awarded to the same MWOB firm to build one of the mission critical systems on the new common platform. Other IT contracts awarded to MWOB firms in 2019 included a $12.7 million contract for audit and risk management support services; three contracts totaling $7.9 million for business intelligence services; and a $1.9 million contract for IT lifecycle consulting services. Lastly, FDIC continues to recognize that IT hardware and software can often be provided by resellers certified by the manufacturer or by MWOB manufacturers. As a result, the FDIC continued with the strategic decision to solicit MWOBs for hardware and software purchases when possible. This strategy resulted in 89 contract awards to MWOBs with a combined value of $19.1 million.

Facilities Management Services

Significant awards to MWOBs in facilities management and security services included contracts valued at $1.9 million for emergency preparedness services; $1.8 million for elevator maintenance services; and $690,092 for construction management services.

In addition, the FDIC continued to provide opportunities to MWOBs for both new and replacement furniture. In total, three contracts with a combined value of $678,927 were awarded to MWOBs to provide furniture for FDIC locations nationwide.

Bank Resolution Contracts

There were only four bank failures in 2019, but there are still many active failed bank receiverships from prior year bank failures. The FDIC continued to award contracts and task orders to MWOBs to provide required services to resolve 2019 bank failures, required services for active receiverships and planning services for future bank failures. In 2019, 30 contracts and task orders with a combined value of $30.4 million were awarded to MWOBs to provide the required financial services to support FDIC’s bank failure processes. Contracts awarded to MWOBs included, but were not limited to: accounting services; receivership assistance services; business and IT development support services; data and media disposition; owned real estate; temporary staffing services; appraisal services; imaging and indexing services; asset sales; asset valuation services; environmental services; tax services and furniture, fixtures and equipment auctions.

Other Significant MWOB Contract Awards

Recognizing the need to expand MWOB contract awards beyond services for bank resolutions, information technology, and facilities management, the FDIC looked for MWOB opportunities in other program areas. The FDIC’s Corporate University awarded four contracts with a combined value of $302,480 to MWOB firms to provide learning and curriculum development services. The FDIC’s Division of Depositor and Consumer Protection awarded a contract valued at $110,000 to an MWOB firm to provide translation services. The Office of Inspector General awarded two contracts with a combined value of $4.1 million to MWOB firms for IT support services and a culture change study. The Office of Minority and Women Inclusion awarded four contracts with a combined value of $94,559 for diversity services.

Outreach to MWOBs

In 2019, the FDIC participated in a combined total of 18 business expos, 6 one-onone matchmaking sessions, and 4 panel presentations. The FDIC and other OMWI agencies presented as panelists during various procurement events including the National 8(a) Small Business Conference and the Annual Government Procurement Conference, educating attendees about doing business with the agencies. Additionally, the FDIC’s Division of Administration, Acquisition Services Branch, attended eight MWOB procurement events. At the various outreach events, the FDIC staff provided information and responded to inquiries regarding the FDIC’s business opportunities for minorities and women. In addition to targeting MWOBs, Minority and Women Owned Investors, and MWOLFs, these efforts also targeted veteran-owned and small disadvantaged businesses. Vendors were also provided with the FDIC’s general contracting procedures and encouraged to register through the FDIC’s CRL.

On December 5, 2019, the FDIC and the other OMWI agencies partnered with the Minority Business Development Agency and the Northern Virginia Procurement Technical Assistance Center to host the “Connections That Count” technical assistance event. The event was held at George Mason University, in Arlington, Virginia. Opening remarks were provided by FDIC’s Deputy to the Chairman and Chief Operating Officer and the FDIC OMWI Director. Technical assistance events are designed to provide information, resources, and tools to MWOBs in order to build and expand federal contracting opportunities. Event highlights included sessions on how to create winning teaming arrangements and former small businesses sharing tools of success for growing business. The featured presenters’ topics were Strategies for Successful Teaming, Blueprint for Growth, and Harvesting Low Hanging Fruit in the Federal Sector. Networking time was allotted for attendees to promote their firms’ technical services to the OMWI Agencies and the Resource Partners. Overall vendor feedback on the event was positive, narrative comments indicated attendees thought the session topics provided valuable insights on the government procurement vehicles; and leading practices to enhance their teaming approach. There were 138 attendees at this event.

FDIC Asset Sales

In its role as receiver, the FDIC Division of Resolution and Receivership manages and sells retained bank assets acquired from failed financial institutions. The assets are sold and proceeds used to pay out depositors and replenish the deposit insurance fund. To promote MWOB participation in FDIC asset sales DRR in collaboration with OMWI host asset purchaser events. These events are marketed extensively to minority- and women-owned investors and companies to raise the awareness and provide information on how to purchase owned real estate (ORE) through DRR’s Owned Assets Marketplace and Auctions Program, as well as other loans and ORE assets from the FDIC, through cash loan sales and structured transactions. These events are generally held in association with failed bank activity. There were no events held in 2019, as there were few bank failures, and the Assuming Institutions which purchased the failed bank franchises also bought nearly all of the assets.

Challenges

As noted earlier, the FDIC’s annual number of new contracts awarded and total contract dollars awarded continues to be significantly lower than during the height of the financial crisis due to the significant reduction in the number of bank failures. From 2009 to 2012, the FDIC’s annual contract awards ranged between $1 billion and $2.6 billion. During this timeframe, up to 85 percent of all contract dollars awarded annually supported bank failure activity. The FDIC has had great success in awarding contracts to MWOBs for bank failure activity as evidenced by the fact that 28.1 percent of the $9.1 billion in contracts awarded in this area since 2007 have been to MWOBs.

In 2019, total FDIC contract dollars awarded were $554.0 million, which represented the fourth consecutive year the total value of new contracts awarded was less than $600 million and the 518 contracts awarded were the fewest contracts awarded since 2008. With only four bank failures, only 15.6 percent of contract dollars awarded supported bank failure activity. Non-financial goods and services contracts for supporting daily operations are continuing to represent a larger percentage of the FDIC’s annual contracts.

The FDIC recognized several years ago that with a declining need for financial services contracts, the FDIC would need to explore MWOB opportunities in other areas. One of the major areas the FDIC has focused on has been contracts for IT goods and services. The majority of the FDIC’s contract dollars awarded (57 percent) in 2019 were for IT goods and services. As a result of the creative ITAS II BOA strategy previously discussed, a focused approach on hardware/software purchases and strategies developed for new contracts awarded in 2019, the FDIC awarded 35.8 percent of all IT contracts and 44.5 percent of all IT contract dollars to MWOBs in 2019.

Despite the FDIC’s MWOB success in IT contracts and financial services contracts, there are a few areas the FDIC has had limited success. The FDIC has several large contracts for employee benefits (dental, life and vision insurance) and the management of the FDIC’s student residence center and cafeterias. The FDIC has conducted expanded and targeted market research and explored new procurement strategies in these areas, but so far, the FDIC has had limited success with these requirements. Unfortunately, these contracts often make up a disproportionate share of the ceiling value of FDIC contracts. In addition, due to the FDIC’s corporate structure with over 80 offices nationwide, some contracts are issued on a nationwide basis to cover all FDIC locations. While smaller firms that are not national in scope are capable of providing some of these services on a local basis, in many cases there are significant administrative advantages to having fewer contractors provide these services to ensure consistent implementation of FDIC programs throughout the FDIC’s 80 plus offices nationwide.

Despite the decline in contract dollars awarded since the financial crisis and the challenges described above, the FDIC through its aggressive outreach program continues to educate and equip MWOBs with the tools they need to compete for contracting opportunities and to have success. These programs resulted in 29 percent of the FDIC’s contracts being awarded to MWOBs and an increase in total contract dollars awarded to MWOBs from 24.5 percent in 2018 to 31.3 percent in 2019. The FDIC will continue to assess and analyze future contracting needs to determine where MWOB opportunities may exist or if new methods of service delivery are feasible.

The FDIC is committed to creating and maintaining a workforce representative of all segments of society. The FDIC’s Diversity and Inclusion Strategic Plan outlines a course for promoting workforce diversity by recruiting from a diverse, qualified group of potential applicants, and cultivating workplace inclusion through collaboration, flexibility, and fairness. In 2005 the FDIC launched the Corporate Employee Program (CEP) program to recruit and train entry-level examiners. The examiner occupational category represents the largest segment of the FDIC workforce and serves as the primary feeder pool for management and senior leadership positions in the agency. During 2019 the CEP program was restructured to further strengthen the agency’s ability to attract, retain, and advance a diverse and more inclusive workplace.

The FDIC began the process in 2019 of updating its Diversity and Inclusion Strategic Plan for the coming years. The next plan will cover 2020 – 2022. This plan incorporates the FDIC’s currently separate Disability Employment Program Strategic Plan so we now have a unified plan. The strategic plan will continue to identify agency strategies to promote increased diversity through the FDIC’s recruiting, hiring, and inclusion practices. The Plan will also continue to ensure the sustainability of the FDIC’s diversity and inclusion efforts by educating leaders with the ability to manage diversity, monitor results, and refine approaches on the basis of actionable data. Specific strategies in the plan will enhance diversity and inclusion at the FDIC through analytics and reporting, training and education, internal and external partnerships, leadership engagement, and accountability. OMWI staff spends considerable time conducting data analysis related to diversity and inclusion workforce metrics. This data analytics work is a part of its affirmative employment program and also in response to requests from the EAC and division and office inquires. The FDIC maintains a diversity and inclusion metrics dashboard which allows for OMWI and agency senior leadership to monitor and report on workforce diversity progress at the division or agency level.

The following sections provide information on current FDIC diversity levels, initiatives to advance diversity and inclusion, as well as challenges the FDIC faces in its efforts to promote greater diversity in hiring and employment.

Diversity in Employment and Hiring

As of December 31, 2019, minorities accounted for 30.4 percent (1,768) of the FDIC’s total workforce (permanent and non-permanent) of 5,821 employees, and women accounted for 44.9 percent (2,613). [See Figure 10.] More specifically, the representation percentages in the total workforce for various minority groups at the end of December 2019 were as follows: 1.7 percent for people of two or more races, 0.6 percent American Indian or Alaska Native (AIAN), 6.4 percent Asian American, 17.4 percent Black American, and 4.2 percent Hispanic American.

Figure 10 Diversity in Total –

(Permanent and Non-Permanent) Employment as of 12/31/2019

| Minority | Non-Minority | Total | |

|---|---|---|---|

| Number | 1768 | 4,053 | 5,821 |

| Percent | 30.4% | 69.6% | 100.0% |

| Men | Women | Total | |

|---|---|---|---|

| Number | 3,208 | 2,613 | 5,821 |

| Percent | 55.1 | 44.9 | 100% |

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |

|---|---|---|---|---|---|---|---|

| Number | 101 | 35 | 374 | 1,011 | 247 | 4,053 | 5,821 |

| Percent | 1.7% | 0.6% | 6.4% | 17.4% | 4.2% | 69.6% | 100.0% |

The racial, ethnic, and gender diversity of the FDIC’s workforce overall has improved since the passage of Section 342 of the DFA. Minorities accounted for 26.2 percent of the FDIC’s permanent workforce as of July 31, 2010, and 30.4 percent as of December 31, 2019. The percentage of women in the FDIC’s permanent workforce was 43.6 percent as of July 31, 2010, and 44.9 percent as of December 31, 2019. [See Appendix C.]

As of December 31, 2019, minorities accounted for 16.7 percent (23) of the FDIC’s total Executive Manager (EM) workforce of 138 employees, and women accounted for 37.7 percent (52). [See Figure 11.]

Figure 11 Diversity in Total (Permanent and Non-Permanent) Employment –

Executive Manager Workforce as of 12/31/2019

| Minority | Non-Minority | Total | |

|---|---|---|---|

| Number | 23 | 115 | 138 |

| Percent | 16.7% | 83.3% | 100.0% |

| Men | Women | Total | |

|---|---|---|---|

| Number | 86 | 52 | 138 |

| Percent | 62.3% | 37.7% | 100.0% |

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |

|---|---|---|---|---|---|---|---|

| Number | 0 | 1 | 3 | 17 | 1 | 115 | 138 |

| Percent | 0.0% | 0.7% | 2.2% | 12.3% | 1.4% | 83.3% | 100.0% |

The racial, ethnic, and gender diversity of the EM workforce overall has increased since the passage of Section 342 of the DFA. The percentage of women in the FDIC’s EM workforce was 25.0 percent as of July 31, 2010, and 37.7 percent as of December 31, 2019. Appendix C depicts the FDIC’s five-year trends for the total, permanent, and EM workforce for 2015 through 2019.

Initiatives to Promote Diversity in Employment

The FDIC promotes its commitment to a diverse workforce through a wide variety of methods aimed at attracting, recruiting, hiring, and retaining high-performing individuals who reflect the diversity of our society. The FDIC’s largest occupational group is bank examiners. The recruitment of entry-level examiners as Financial Institution Specialists (FIS), had been conducted primarily through the CEP.

After a thorough study of processes for recruiting, hiring, and training examiners, in 2019 the FDIC implemented structural changes to the CEP, creating a new entry-level examiner hiring program to support examiners and supervisory efforts and to ensure future readiness. This included the creation of an executive level taskforce to evaluate and strengthen the agency’s ability to attract, retain, and advance a diverse pool of candidates, facilitating a strong, diverse, and more inclusive workplace.

OMWI tracked and informed FDIC leadership about the representation and attrition rates for CEP participants based on race, ethnicity, and gender. Reports on participation rates were prepared following incoming classes of CEP hires, and each report included the total participants from the inception of the program, FISs currently onboard, and attrition information. OMWI will track hiring, attrition, and other aspects of the employment lifecycle for participants of the new entry-level examiner hiring program to evaluate impacts on diversity and inclusion.

The FDIC has engaged in a proactive recruitment effort using recruitment strategies that have improved the representation of several, racial, ethnic, and gender groups in the examiner workforce since the inception of the CEP. The overall percentage of women in the examiner workforce increased from 33.5 percent as of December 31, 2004, to 39.2 percent as of December 31, 2019. In addition, the percentages of Black American men and women, Hispanic American women, Asian American men and women, American Indian or Alaska Native men and women, and White women in the overall examiner workforce all have increased since the beginning of the CEP. However, despite the positive progress in those areas, the representation rates of Hispanic American men and women, Asian American men and women, Black American women, and women of two or more races in the FDIC’s examiner workforce remain below the Civilian Labor Force (CLF) benchmark for the occupational series.

Since the inception of the CEP, overall hiring rates have been at or above the percentages in the CLF for men and women of two or more races, American Indian or Alaska Native men and women, and Black American men and women, but lower than the CLF for Asian American men and women, Hispanic American men and women, and White women. [See Figure 12.] The overall minority hiring rate since the inception of the CEP has been 27.5 percent; and the overall hiring rate for women has been 39.3 percent.

| Figure 12 CEP Hires Since Inception | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |||||||

| Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | ||

| CEP | 21 | 23 | 5 | 12 | 44 | 67 | 192 | 125 | 39 | 53 | 528 | 1,000 | 2,109 |

| % | 1.0% | 1.1% | 0.2% | 0.6% | 2.1% | 3.2% | 9.1% | 5.9% | 1.8% | 2.5% | 25.0% | 47.4% | 100.0% |

| CLF | 1.0% | 0.6% | 0.2% | 0.1% | 3.7% | 3.5% | 8.4% | 3.4% | 3.7% | 3.1% | 28.3% | 44.1% | 100% |

During 2019, CEP hiring rates were above the CLF percentages for men and women of two or more races, American Indian or Alaska Native men and women, Asian American men, Black American men, Hispanic American men, and White women, and were below the CLF for Asian American women, Black American women, Hispanic American women, and White men. While the hiring rate for White men was below the CLF, historically White men have been above the CLF for CEP and continue to be represented above the CLF within the examiner workforce. [See Figures 13 and Appendix D] The overall hiring rate in 2019 for minorities and women was positive.

| Figure 13 CEP Hires in 2019 (Classes 63-73) | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |||||||

| Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | ||

| CEP | 4 | 2 | 1 | 1 | 3 | 8 | 10 | 8 | 2 | 8 | 52 | 63 | 162 |

| % | 2.5% | 1.2% | 0.6% | 0.6% | 1.9% | 4.9% | 6.2% | 4.9% | 1.2% | 4.9% | 32.1% | 38.9% | 100% |

| CLF | 1.0% | 0.6% | 0.2% | 0.1% | 3.7% | 3.5% | 8.4% | 3.4% | 3.7% | 3.1% | 28.3% | 44.1% | 100% |

As a significant component of the recruitment strategy for entry-level examiners, FDIC recruiters participated in job fairs aimed at targeted professional audiences and maintained ongoing relationships with a wide range of colleges and universities. This includes 115 institutions designated as Hispanic Serving Institutions, Historically Black Colleges and Universities (HBCUs), and other minority-serving institutions, tribal colleges and universities, and institutions with significant student populations of women, and minorities.

With regard to targeting professional audiences, in 2019, FDIC recruiters attended 19 national diversity outreach events and seven regional outreach events to increase awareness of the FDIC as an employer of choice to professionals. The FDIC also met with key leaders in Hispanic American, Black American, Asian American, women’s, and veterans’ organizations as well as organizations representing people with disabilities to create awareness of FDIC careers and identify opportunities to expand outreach to their members. For example, the FDIC participated in the National Association of Black Accountants (NABA) 2019 National Convention & Expo and the Hispanic Association of Colleges and Universities (HACU) 33rd Annual Conference.

With respect to recruiting students (both traditional and non-traditional), FDIC corporate recruiters participated in 285 college career fairs, 11 information sessions, and other recruitment-related campus activities throughout the United States to brand the FDIC and attract qualified candidates. Recruitment efforts during 2019 also included the following:

- Hosted developmental workshops for students and entry-level professionals at events for professional affinity groups:

- Personal Branding (2019 Thurgood Marshall College Fund (TMCF) Leadership Institute & Recruitment Fair)

- Vision, Leadership + Value: Build a Platform with your Voice at the Center HACU 33rd Annual Conference;

- Managing IT Risk in a Changing Environment (Association of Latino Leaders for America (ALPFA) 2019 Convention);

- Leadership Networking: Cultivating Authentic Connections to Accelerate Your Career (Prospanica 2019 Annual Conference & Exposition); and

- Personal Branding (2019 ALPFA Northeast Regional Symposium in Boston)

- Conducted informational interviews and provided application assistance at the following: ALPFA, HACU, Prospanica, and TMCF.

- Conducted federal resume review at Prospanica.

To assist in increasing participation rates for underrepresented groups in the non-examiner occupations, the FDIC’s recruitment strategy includes outreach to prospective applicants for entry-level positions in these occupations throughout the agency. These efforts led to increased level of minority representation within the economist occupation at FDIC, which continues. The FDIC’s Division of Insurance and Receiverships (DIR), where the majority of the FDIC’s economists reside, continued its partnership with Delaware State University to improve the diversity pipeline of applicants for Economic Research Assistants and intern positions. In 2019, DIR expanded outreach efforts to two other HBCUs, Howard University and Morgan State University.

DIR continues to use an alumni log for Economists, Economic Analysts, and Economic Research Assistants to cultivate and strengthen diversity outreach for entry-level positions through alumni relationships with universities and colleges. The log has served as a reference tool for DIR recruiters when attending outreach events and career fairs at universities across the U.S. The FDIC also conducted outreach to minority and women professional economist organizations to gain access to listservs or distribution networks that might expand FDIC’s pipeline to qualified Economic Research Assistants and interns. Additionally, the division plans to participate in the American Economic Association Summer Fellowship Program, which targets women and minorities with PhDs.

In 2019, the FDIC and NTEU reached a new compensation agreement that included a Pilot Student Loan Repayment Program, which will assist in recruitment and retention efforts.

Diversity and Inclusion Analytics Dashboard

The FDIC’s workforce analytics dashboard provides actionable data to senior leadership on the FDIC workforce by gender and minority status, and by division and office, region, race, ethnicity, occupation, grade level, and employment type (permanent and non-permanent). This information supports the evaluation of diversity and inclusion efforts at all levels of the organization. Trends measure progress and facilitate the development of strategies or the adjustment of plans where needed. In 2019, each division used information from the dashboard to help drive diversity and inclusion strategic plans at the division level. The FDIC will continue to identify additional enhancements to the dashboard that will permit senior leaders to continue understanding and advancing diversity and inclusion within their organizations.

Inclusion Initiatives

The FDIC continues to engage in initiatives to support inclusion and retention efforts within the corporation, and the FDIC’s Diversity and Inclusion Education Series is an integral component of building workforce inclusion. Annually, OMWI hosts 10 corporate-wide observances as part of its education series. The education series raises cultural awareness and fosters an environment of cultural intelligence, providing a safe space to share histories and experiences.

In 2019, the FDIC continued to leverage the Chairman’s Diversity Advisory Councils (CDACs) to integrate diversity and inclusion efforts throughout the agency. The CDACs were established to assist the OMWI to break down barriers, increase awareness of cultural differences, and promote inclusion and collaboration among all employees. The CDACs are comprised of six regional and a headquarter council, with a maximum of nine members per council and, to the extent possible, reflects the general composition of the FDIC’s diverse labor force (i.e., different grade levels, positions, and bargaining and non-bargaining status).

The CDACs’ mission is to provide advice to the FDIC’s Chairman, through the OMWI Director, on any diversity-related issues and concerns. Its objective is to recommend changes in corporate policies and procedures that would foster the FDIC’s diversity and inclusion goals and strategies. One of the issues the CDACs raised in 2018 was paid parental leave. The FDIC’s new compensation agreement with the NTEU in 2019, included six weeks of paid parental leave for the birth, adoption, or foster care of a child.

The councils also assisted and worked with OMWI to sponsor programs that address cultural diversity and promote initiatives that acknowledge and recognize the benefits of the diverse heritages and cultures that exist throughout the corporation. The CDACs held a combined total of 81 events on a variety of diversity and inclusion topics, including but not limited to: nationally recognized observance months, “Generational Diversity in the Workplace”, “Supporting Transgender Rights”, disability awareness, unconscious bias, and inclusiveness.

The FDIC’s Chairman and senior management have strongly supported the CDACs’ initiatives. The programs and activities sponsored by the CDACs have brought employees together to demonstrate how diverse backgrounds bond individuals to strengthen the FDIC’s mission and goals, and have taken place nationwide at various FDIC offices.

The FDIC also continues to engage with its nine ERGs. ERGs are FDIC-recognized networks of FDIC employees with common goals, interests, or life experiences. The FDIC started the ERG Program to foster and encourage equality of opportunity, respect, and fair treatment for all. ERGs are vital to the FDIC’s ability to create and maintain a culture and environment that recognizes, appreciates, encourages, and utilizes the talents, skills, and perspectives of all employees in order to achieve the FDIC’s mission.

OMWI staff regularly meets with the ERGs to discuss programs and issues. Among other initiatives, in 2019, the ERGs partnered with the Washington CDAC to host an ERG Open House to provide employees an opportunity to meet ERG representatives and learn more about the nine ERGs recognized by the FDIC.

In 2020, the FDIC plans to participate in the Marion S. Barry Summer Youth Employment Program in partnership with the Office of the Comptroller of the Currency (OCC) and the District of Columbia (DC) Employment Office. Interns will be exposed to various work experiences and participate in numerous enrichment activities. In accordance with the Dodd-Frank Act, the FDIC, joining with the OCC, can provide promising opportunities for high school students, thereby improving their chances of future success.

Challenges

A key challenge for the FDIC in promoting diversity at all levels of its workforce continues to be the representation of minorities and women in its bank examiner workforce. The examiner occupation represents the largest occupational group at the FDIC and accounts for 46.6 percent (2,715) of the FDIC total workforce (5,821). Individuals who began their FDIC careers as entry-level examiners tend to occupy a significant percentage of executive and managerial leadership positions at the agency, as well as other non-examiner positions in the FDIC. Thus, representation rates within the examiner workforce are key elements to achieving satisfactory representation rates within the broader FDIC workforce.

The FDIC’s Financial Management Scholars Program (FMS), has assisted in the diversity of the examiner ranks. The FMS program is an 11-week paid summer internship program for highly-qualified college students. At the end of the program, qualified FMS interns receive post-graduation employment offers with the FDIC. The FMS program continues to hire, in aggregate, above the CLF for women since the inception of the program in 2011. Participation for minorities in the FMS program over the life of program remained below the CLF but continues a steady increase.

Despite the overall success of the CEP in increasing the percentage of minorities and women in the examiner workforce, those percentages still remain below the CLF for certain groups such as for Asian American men and women, Hispanic American men and women, and Black American women, and women of two or more races. The FDIC continually works to ensure that recruiting sources, hiring decisions, interviewing processes, training activities, retention efforts, and advancement pools reflect a purposeful and intentional effort to leverage the power of diversity to maintain a high performing examination workforce. A key challenge for the FDIC in promoting diversity at all levels of its workforce continues to be the ability to attract, retain, and advance minorities and women in its bank examiner workforce.

From 2005 until 2019, the FDIC hired entry level examiners as FIS through the CEP. With increased retirements anticipated in the near future, and gaps in the succession pipeline, the FDIC must identify and prepare future leaders now to fulfill roles in the years to come, while concurrently seizing the opportunity to continue to mold the diversity of the FDIC. The FDIC also recognizes that maintaining an inclusive work environment is critical for minimizing attrition and maintaining diversity.

In 2019, the FDIC closely reviewed current processes, historical and current data, business and staffing needs, time and resource challenges, and costs for hiring entry level examiners. The FDIC created an executive level taskforce, which includes the OMWI Director, to strengthen its ability to attract, retain, and advance a diverse pool of examiner candidates. The taskforce conducted a high level review of available data from OMWI, identified key challenges and made several recommendations to mature the diversity and inclusion model for the examination workforce. It is anticipated that these recommendations will result in several actions being taken during 2020 and beyond.

OMWI supports the taskforce by providing actionable data to help build a results driven diversity and inclusion strategy. Also, OMWI will also track hiring, attrition, and other aspects of the employment lifecycle for participants of the new entry-level examiner hiring program to evaluate impacts on diversity and inclusion. [See Figure 14.] The first group of examiners under this new program are scheduled to onboard in early 2020.

| Figure 14 CEP Attrition Rates | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total | 2 or More | AIAN | Asian | Black | Hispanic | White | |||||||

| Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | ||

| Hired | 2,109 | 21 | 23 | 5 | 12 | 44 | 67 | 192 | 117 | 39 | 53 | 528 | 1,000 |

| Involuntary Departures | 41 | 0 | 0 | 0 | 0 | 1 | 1 | 8 | 9 | 1 | 2 | 4 | 15 |

| Involuntary Attrition Rate+(%) | 1.9% | 0.0% | 0.0% | 0.0% | 0.0% | 2.3% | 1.5% | 4.2% | 7.2% | 2.6% | 3.8% | 0.8% | 1.5% |

| Subtotal | 2,068 | 21 | 23 | 5 | 12 | 43 | 66 | 184 | 116 | 38 | 51 | 524 | 985 |

| Voluntary Departures | 744 | 5 | 2 | 1 | 5 | 17 | 31 | 71 | 57 | 14 | 16 | 178 | 347 |

| Voluntary Attrition Rate *(%) | 36.0% | 23.8% | 8.7% | 20.0% | 41.7% | 39.5% | 47.0% | 38.6% | 49.1% | 36.8% | 31.4% | 34.0% | 35.2% |

| Number Retained | 1,324 | 16 | 21 | 4 | 7 | 26 | 35 | 113 | 59 | 24 | 35 | 346 | 638 |

| + “Involuntary Attrition Rate” is the Involuntary Departures divided by the total hired. * “Voluntary Attrition Rate” is the Voluntary Departures divided by the subtotal. | |||||||||||||

In the non-examiner occupations of economists, financial administration, accountant and auditors, attorneys, and general business and industry, the FDIC continues to face the challenges in attracting and recruiting minorities and women, primarily due to low labor force representation rates for minority groups and women in these occupations. [See Appendix D.]

Despite these challenges, representation of minorities within the economist occupation remains above the relevant CLF, with Hispanic American men, Black American women, and Asian American men and women having higher participation rates than the benchmark. Black American men fall below the CLF. Hispanic American women, American Indian or Alaska Native men and women, and men of two or more races are absent. Overall, women fall below the CLF within the economist occupation, with Hispanic American women and White women showing the greatest differences from the benchmark.

In the financial administration and program occupation, minorities overall are above the relevant CLF. However, Hispanic Americans fall below the CLF. American Indian or Alaska Native men and women of two or more races are absent in this occupation. Additionally, women overall, particularly White and Hispanic American women fall below the CLF.

For the accountant/auditor occupations, Hispanic American men, American Indian or Alaska Native men and women are absent. Compared to 2018, there has been improvement in the representation of Hispanic American women and women of two or more races. White women and Asian American men have a low representation compared to the relevant CLF for the accountant and auditor occupation. In aggregate, minorities continue to remain above the CLF benchmark for this occupation while women are below.

In the attorney occupation, minorities in aggregate are above the CLF. However, some groups of minorities have participation rates slightly below the relevant CLF in the attorney occupation, including Hispanic American men and women and Asian American men. Women overall are above the CLF, while men overall are below. Women of two or more races are absent in this occupation.

Women overall, including those in all racial/ethics groups, fall below the CLF in the general business and industry occupation. All groups of men are above relevant CLF for this occupation.

In 2019, the FDIC continued monitoring race, ethnicity, gender, and grade levels by FDIC divisions and offices. OMWI met with various agency divisions and offices to discuss representation and strategies for expanding outreach and recruitment more broadly to increase minority and women representation within major occupations and at senior levels within the FDIC. In the coming year, OMWI will continue to engage with agency divisions and offices to assist in advancing diversity and inclusion, in alignment with strategies and action items outlined in the FDIC Diversity and Inclusion Strategic Plan.

The information in this section discusses FDIC activities that pertain to other relevant programs and successes that support provisions of Section 342 of the DFA. The FDIC demonstrates commitment to business diversity by assessing the diversity policies and practices of regulated financial institutions; verifying contractors’ commitment to workforce diversity; and promoting the economic inclusion and development for lowand moderate income communities.

OMWI administers both the Financial Institution Diversity and Contractors’ Workforces Fair Inclusion programs. The programs promote diversity and inclusion practices and procedures among FDIC–regulated financial institutions and contractors. The annual self-assessment submitted by FDIC-regulated financial institutions identify diversity and inclusion practices that financial institutions have implemented. Interagency Policy Statement Establishing Joint Standards for Assessing the Diversity Policies and Practices of Entities Regulated by the Agencies, the Standards offer guidance and a framework for assessing diversity practices, examining leadership commitment, reporting on workforce metrics, and taking affirmative actions to improve workforce and supplier diversity. The assessments have enabled OMWI to identify industry trends and exemplary practices financial institutions have implemented.

Also, the FDIC provides technical assistance and outreach to low-and moderate income communities. The Community Affairs Program, through partnerships with banks, government entities, and community organizations promotes access to affordable credit and deposit services in these historically underserved communities. The FDIC efforts encourage responsible options for affordable mortgage credit; promote affordable insured transactions and savings accounts; strengthen access to financial services for small businesses; increase consumer access to sustainable credit; and support financial education and literacy. In addition, the preservation and promotion of minority depository institutions (MDI) remains a long-standing and high priority for the FDIC. In 2019, the FDIC expanded engagement with MDIs and continued to promote and support MDI and Community Development Financial Institution (CDFI bank) industry-led strategies to better serve their communities.

Financial Institutions Diversity

Section 342 of the DFA requires FDIC to report on the data received from their respective regulated institutions annually to Congress. The FDIC conducts analysis of the self-assessment information and highlights exemplary diversity and inclusion practices for the purpose of assisting financial institutions benchmark and strengthen diversity programs. A report on the self-assessments analysis is posted on the FDIC’s website and shared with financial institutions in order to leverage industry trends and leading practices in diversity and inclusion. Since the first reporting period in 2016, 365 financial institutions have reported on diversity practices.

In early 2017, the FDIC obtained approval from the Office of Management and Budget (OMB) to collect assessment information from regulated entities to assist and strengthen diversity programs in financial institutions through a self-assessment instrument. The instrument provides the framework for regulated financial institutions to assess and strengthen diversity policies and practices, and covers the following areas derived from the Policy Statement:

- Organizational Commitment to Diversity and Inclusion

- Workforce Profile and Employment Practices

- Procurement and Business Practices – Supplier Diversity

- Practices to Promote Transparency of Organizational Diversity and Inclusion

- Entity’s Self-Assessment

The FDIC-regulated financial institutions began voluntarily submitting diversity selfassessments to the FDIC’s OMWI for the 2016 reporting period. The results of the 2016 analysis established the baseline for subsequent reporting periods. The completed analysis is posted on both internal and external web-site3.

3. See https://www.fdic.gov/about/diversity/dibanking.html.

In January 2019, the FDIC’s OMWI Director distributed a letter to the Presidents and Chief Executive Officers of 784 FDIC-regulated financial institutions identified as having 100 or more employees. The letter informed these institutions about the process for conducting and voluntarily submitting their diversity information to the FDIC. The OMWI Director issued a reminder letter in March 2019, to financial institutions to encourage participation, and extended the submission deadline to April 2019. The FDIC received diversity self-assessments from 133 (16.9 percent) of its regulated financial institutions.

There was an increase from the 2016 reporting period (95 financial institutions) to the 2017 reporting period (137 financial institutions). There was a slight decrease for the 2018 reporting period to 133 from 137 financial institution submissions; however, the percentage of self-assessments received increased in 2018.

The chart below illustrates a comparison of responding FDIC-regulated financial institutions for the 2016 to 2018 reporting periods.

| Comparative of Responding Financial Institutions | |||||

|---|---|---|---|---|---|

| Reporting Period | # Financial Institutions (Invited) | # Self- Assessments Received | % Self- Assessments Received | # Acknowledged Non-Respondents | # Minority Depository Institutions |

| 2016 | 805 | 95 | 11.81 | 2 | 10 |

| 2017 | 820 | 137 | 16.71 | 3 | 8 |

| 2018 | 784 | 133 | 16.96 | 3 | 7 |

The FDIC completed an analysis of the financial industry’s diversity policies and practices for the 2018 reporting period and a comparative analysis against the 2016 and 2017 reporting periods, for the purpose of monitoring progress and trends of diversity and inclusion in employment and contracting activities. The analysis further provided the opportunity to identify exemplary diversity policies and practices.

Overall, OMWI has observed that the reporting results have remained consistent over the last two reporting periods, for 2017 and 2018. The FDIC is exploring ways to increase its outreach efforts to further encourage and guide its regulated financial institutions to implement policies and practices, and share their completed selfassessments to further raise awareness aiming to improve levels of diversity and inclusion throughout the financial industry.

Workforce Profile